For the majority of working income earners in America, there is a trusty pattern we have been practicing since grade school. It goes something like this:

- Monday: First day back at work from the weekend

- Tuesday: When you actually start getting work done for your week, aka: second Monday

- Wednesday: Hump day

- Thursday: the weekend is in sight

- Friday: wrap up the work week and prepare for the weekend

- Saturday and Sunday – your time

Even people who work 6 or 7 days a week and multiple types of shifts share a common foundation of the 7 day week.

When most of us start to think about revamping our budget, the first response may be to think by the month: “How much do I make each month and what are my monthly expenses?” When we do that, we may risk working against our well established weekly pattern and could be undervaluing how difficult it may be for us to create a new (monthly) pattern.

And money management is not something that needs to be more difficult.

What is wrong with managing our money using a monthly view? It is wise to take a monthly view, and a yearly view and even longer views of our money. The problem is, if a month is the shortest time view of money we have taken, we haven’t really gone short enough. We are missing an opportunity to incorporate money management into our already well-traveled pattern of the days of the week.

Here are a few steps to take to go about reorganizing their perspective on money management from monthly to weekly:

- Use your calendar. To best understand what is happening with your budget, you need to take a visual look at it. This is very easily accomplished by picking up a wall calendar and writing on it. Start with a blank calendar, go to the dates you get paid each month and write in the payment amounts. Next go through your bills and expenses and write out each expense on the date you usually pay it. This allows you to compare your paycheck to your bills do and see if you may have any due date compatibility issues. It may be possible for you to change your due dates, or you might need to make a plan to save money from one pay period to cover expenses during another pay period.

[Download Our Printable “Take Control of Your Money” Printable Packet TCOYM Combined PDF ]

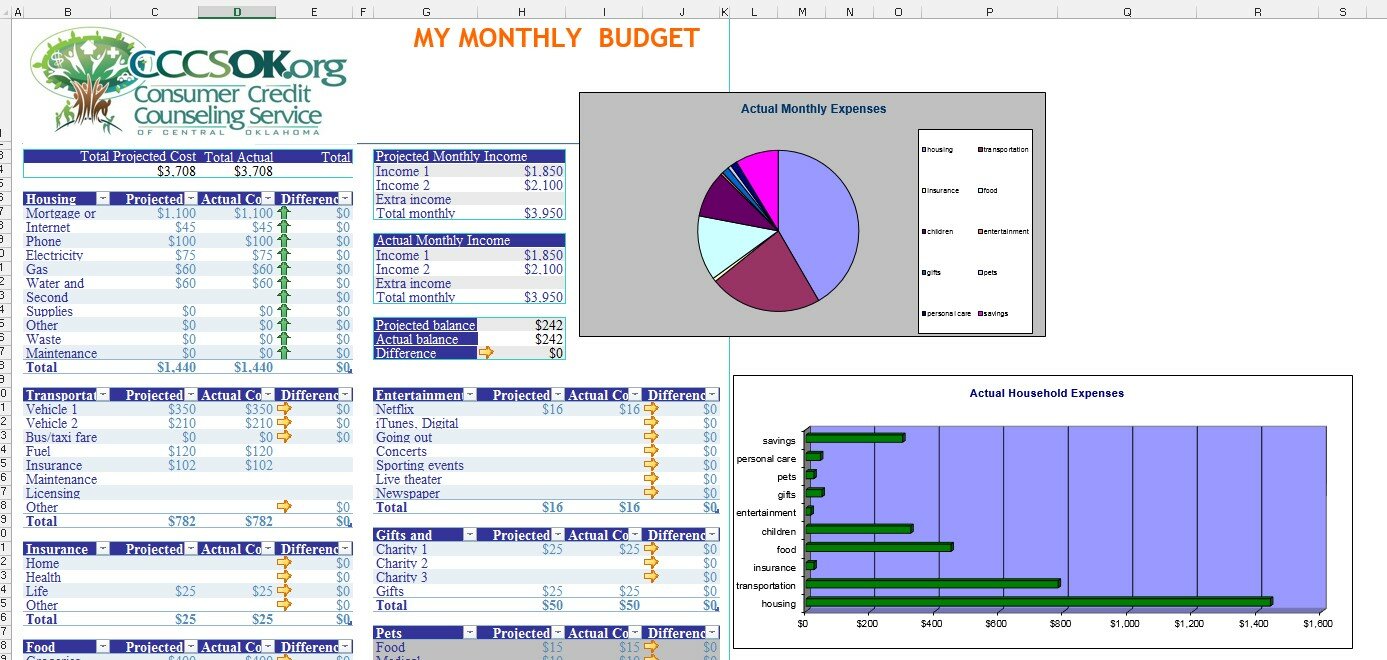

- Build your monthly “Monthly Master Budget”: After you have made some adjustments to your calendar and plan, complete your Monthly Master Budget Template. This template allows you to transfer the information on your calendar to a template that will help you analyze the areas you spend money. You will also be able to see if you have overages or if your budget is unbalanced. This template is designed to help you project what you think your budget is going to be and to let you compare how you actually did with what your plans were so you can make adjustments over time. You can change the names of categories if that will help you.

[Downloadable: My-Monthly-Budget-Template1]

- Make your weekly spending plan: After you have completed your calendar and your master budget, you will have gained valuable confidence and understanding of your budget. Now it is time to build your maintenance plan. Here are a couple of ideas about budgeting that most of us can identify with:

We all have a pretty good idea of what we are going to receive and spend every month for the upcoming future, assuming we have a regular paying job.

At the root, better budgeting is really all about remembering the expenses we usually forget and corralling them into our plan.

This is where the Weekly Cashflow Spending Plan comes in. We use our assumption that our finances are fairly predictable and we plan how we think each week is going to go into the coming year. Predict your income, your savings, and your expenses and place each in the week it will actually happen.

Let’s talk a little about this spreadsheet: The top two lines are the week you are on and the running total, which is the amount of money you have left after your weekly income and expenses. The next section below these two lines is the INCOME section. Here is where you list all types of income. You put the amount of income you will receive during the week you will receive it. Some of those weeks will likely have no income so for those weeks your income section is left blank.

The section below income is a list of all your expenses. Place each expense in the week it will be spent. Review your spending records to see if there is anything you have forgotten so you can get a plan for it now.

[Picture: Shot of filled out Spreadsheet]

[Downloadable: Weekly Cashflow-Spreadsheet NEW: Updated examples for 2015-2016]

Build this out for the next several months – 6 months to a year – and take a look at your year! You may be able to see some upcoming difficulties you can plan for by saving overages from previous weeks.

Your plan is made, so now it needs maintained. Our behavior almost never matches our plans perfectly, so you need to update your plan with what actually happened. This is where you find opportunity for increasing your savings. Each week, pick a day and make a date with yourself to update your plan with your income and spending activities for the week. You won’t need more than 20 minutes after you get your system down. This helps you get in touch with your money at a more realistic level. You may be able to more easily find areas you can reduce spending, and may find ways to redirect a few dollars here and there to boost your savings, helping you to build a better emergency fund.

Using this method helps reduce stress, increases better communication about money with couples, and helps you prepare for emergencies before they happen.

If you need a little help learning how to manage weekly and the example seems too difficult, try this Personal-Cashflow-Budget-Planner It includes tutorials along the side of the spreadsheet to help.

If you would like to have some help in using any of these tools or methods to get the right budget for you, please contact us for a free financial analysis and budgeting session. We will be happy to help you become stronger at managing your finances!