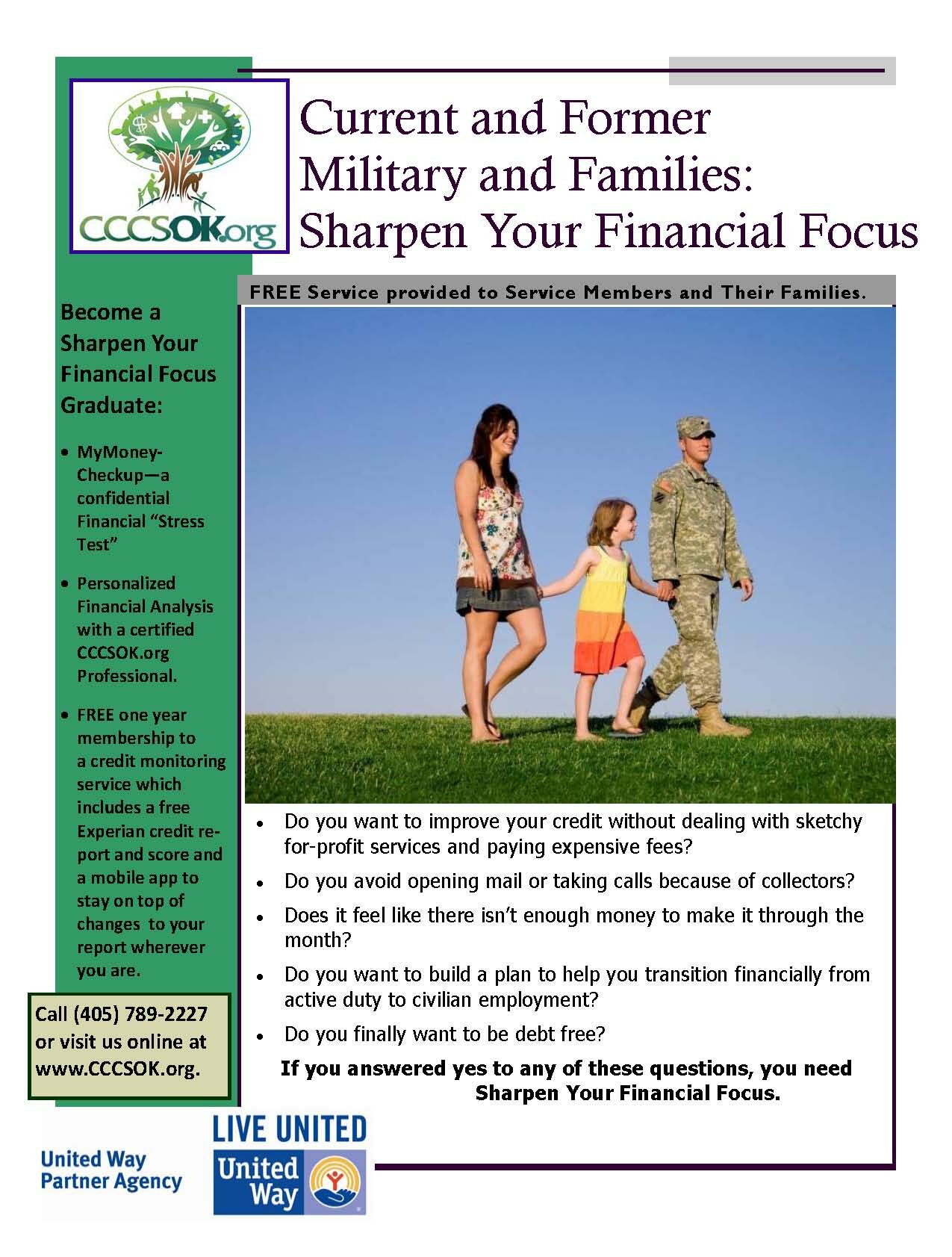

National Foundation for Credit CounselingⓇ (NFCCⓇ) and Ohio State University (OSU) Study Reveals Unique Financial Challenges Faced by the Military.

Bethany, OK – Active members of the military, veterans, and their families are routinely facing complex challenges in their daily lives. Thankfully, there is a growing awareness of the benefit that support networks can play in helping our heroes tackle serious medical, logistical and transitional issues. CCCSOK.org, a member of the National Foundation for Credit CounselingⓇ (NFCCⓇ), recognizes that debt management and savings are matters of common concern among civilians as well as service members and their families.

“Those who serve our country as members of the armed forces are faced with unique circumstances that can influence the financial choices they make,” said Cristy Cash, Vice President with CCCSOK.org. “Our network of member agencies is proud to provide professional resources to guide military members and their families through financial matters during all stages of military life.”

Military participants surveyed after enrolling in the Sharpen Your Financial FocusTM (Sharpen) program of the NFCC were found to have fewer tangible assets and a higher level of unsecured debt than the average program participant. Unsecured debt balances for members of the military averaged 7.1% higher than the combined average according to The Ohio State University (OSU) data. Tangible assets for military consumers were 16.2% less than the overall program participant average. This concerning mix of lower accumulation of wealth and higher than average unsecured debt, combined with the ever changing nature of military life, can create a difficult and dangerous financial cycle.

Programs like Hands on Banking® for the Military, offered by Wells Fargo and the NFCC, provide education and assistance to keep military families on the right track toward financial stability in all stages of military life.

CCCSOK.org has identified the following aspects of military life that pose challenges to personal financial management:

Frequent Relocation – With each move, military families are presented with new housing choices and a different local economy to consider. Length of time at a duty station, employment  options for spouses, and cost of living are all factors that can have a significant impact on household budgets and savings plans.

options for spouses, and cost of living are all factors that can have a significant impact on household budgets and savings plans.

Employment for Military Spouses – A single income is often not enough to make ends meet, however the changing local economy and the cycle of relocation make it nearly impossible for spouses to maintain steady employment. Carefully planning a budget to operate on a single income when necessary is the key to balance income and expenses while avoiding unnecessary reliance on debt.

Deployment – Deployed members of the military are protected from a pileup of interest and fees on existing debts through the Soldiers’ and Sailors’ Civil Relief Act (SSCRA, also known as the Service-Members’ Civil Relief Act or SCRA). Although this protection can cap annual interest rates at 6 percent during deployment, it only applies to debt incurred before beginning active duty and requires a written request for relief to the lender. Responsible debt management that prevents further balance increases is an important consideration for deployed service members and their families on the home front.

Transition to Civilian Life – Employers are encouraged to hire military veterans for a number of good reasons. Former service members are among the best trained and most highly skilled employees available in today’s workforce. With all of the advantages of a distinguished military record, there can still be a few bumps along the way during the move from active duty to civilian life. Changes in salary and housing expenses can pose their own challenges that may require some reliable advice from objective sources.

The NFCC stands ready to serve active duty members of the military, veterans, and their families as they face these unique crossroads in their lives. CCCSOK.org is able to provide financial counseling in-person, by phone, or online. To reach a certified financial counselor today, consumers can call 405-789-2227 or visit CCCSOK.org.

About CCCSOK.org: CCCS of Central Oklahoma (CCCSOK.org) is the oldest and largest non-profit credit counseling agency serving the state of Oklahoma. We are a United Way partner agency and a member agency of the National Foundation for Credit Counseling. We have been serving Oklahomans since 1967 having assisted thousands of families in resolving their delinquent mortgages through our free housing counseling. Thousands of Oklahomans have experienced the relief of repaying over half a billion dollars in credit card debt through our Debt Management Plan. In addition to these services we have helped thousands upon thousands over years and years with our free counseling to reduce stress and get a personalized plan to finally become the CEO of their household money.

See how services from CCCSOK.org can help you: https://www.youtube.com/watch?v=kdqvI1UtJQ4

About the National Foundation for Credit Counseling

The National Foundation for Credit Counseling (NFCC), founded in 1951, is the nation’s largest and longest serving national nonprofit financial counseling organization. The NFCC’s mission is to promote the national agenda for financially responsible behavior, and build capacity for its members to deliver the highest-quality financial education and counseling services. NFCC members annually help millions of consumers through more than 600 community-based offices nationwide. For free and affordable confidential advice through a reputable NFCC member, call (800) 388-2227, (en Español (800) 682-9832) or visit http://www.nfcc.org.